Nigeria Tax

Nigeria 0% CIT Threshold 2026: Calculator, Rates, and Filing Rules

A practical 2026 guide to the Nigeria 0% CIT threshold calculator, corporate income tax rates, minimum tax, late-filing penalties, exempt income, and salary tax examples.

Nigeria 0% CIT Threshold 2026: what this guide answers

Most people looking up the Nigeria 0% CIT Threshold 2026 are not searching for theory. They are trying to answer practical questions fast: are we in the 0% branch, what rate applies if we are not, what penalties apply if filing slips, and what evidence must be kept. This article answers those questions in one place so finance teams, founders, and advisors can align before deadlines.

The structure follows a simple path. First we explain how the Nigeria 0% CIT threshold calculator should be used. Then we cover company income tax rate in Nigeria 2026, how to calculate Company Income Tax, minimum corporate income tax, late filing penalties, exempt-income treatment, and salary tax context for common payroll questions.

You should still treat this as educational guidance. Final filing positions should be validated against enacted law, authority circulars, and professional advice for complex scenarios such as mixed-sector revenue, group restructuring, or significant one-off transactions.

Nigeria 0% CIT threshold calculator: how to use it correctly

The calculator is built for first-pass classification, not blind filing. It asks for three inputs because each serves a separate purpose: annual turnover, business sector, and assessable profit. Turnover and sector decide branch direction. Assessable profit is used only when the levy branch is active.

In this tool implementation, turnover at or below NGN 100 million and a non-Professional Services sector produces an ELIGIBLE FOR 0% CIT screening output. If turnover is above NGN 100 million, the model estimates development levy at 4% multiplied by assessable profit. That estimate is sensitive to the quality of the assessable-profit figure.

Always attach a short assumptions note to each run. Include the source period for turnover, why the sector was selected, and whether assessable profit is final or provisional. That one-page note often saves hours during audit or adviser review.

- Turnover and sector drive branch decision.

- Assessable profit drives levy estimate where branch is active.

- A dated assumptions note converts output into a review-ready record.

Company Income Tax rate in Nigeria 2026: how to read the rates safely

A frequent question is, how many percent is CIT tax in Nigeria. The safe answer is that you must anchor the response to the exact law and assessment year your company is using. Legacy CITA references commonly show turnover-based outcomes that include 0%, 20%, and 30% treatment bands. Those are still widely quoted in templates and advisory decks.

At the same time, this site's 2026 screening model is intentionally scoped to the rules configured in the tool: a 0% branch for qualifying entities up to NGN 100 million turnover when sector condition is met, and a 4% levy estimate path above that threshold. That model is excellent for triage but should be reconciled to current legal text before filing.

If management needs one slide, present both perspectives together: the operational model output and the legal-reference basis for final compliance. This avoids conflicts between dashboard logic and filing calculations.

- Do not quote one CIT percentage without stating legal basis and year.

- Legacy references often include 0%, 20%, and 30% turnover-linked bands.

- This tool uses a specific 2026 screening model for decision support.

How to Calculate Company income tax in Nigeria: step-by-step

A practical calculation workflow starts with accounting profit, then adjusts for tax treatment to derive total profits, assessable profit, and taxable profit under your governing framework. After that, apply the correct CIT branch or rate and compare against minimum-tax rules where required. Skipping any step can produce a polished but wrong number.

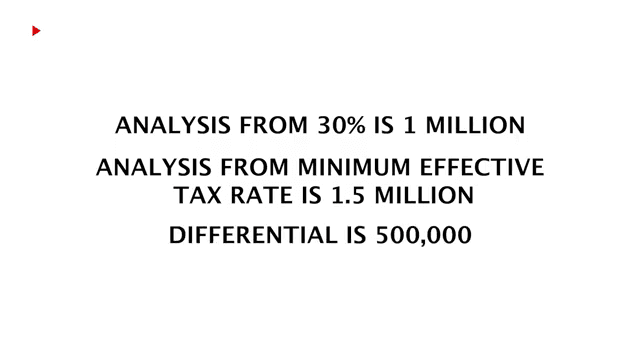

Worked example one: turnover NGN 82 million, sector not Professional Services, assessable profit NGN 18 million. Under this suite's model, the case stays in the 0% CIT screening branch. Worked example two: turnover NGN 150 million and assessable profit NGN 40 million. Development levy estimate becomes NGN 1.6 million using 4% multiplied by assessable profit.

If your numbers are still moving, run scenario bands. A range-based output is more honest and more useful than one precise figure built on incomplete ledgers.

- Start with clean tax-adjusted profit working.

- Confirm turnover basis and sector substance before applying rates.

- Run sensitivity ranges where assessable profit is provisional.

How much is the minimum corporate income tax?

Minimum tax is a control floor that can apply even where normal CIT appears low. In widely used Companies Income Tax Act references, practitioners often apply 0.5% of gross turnover less franked investment income, subject to statutory exceptions and commencement-period rules. Missing those exceptions can lead to overstatement.

The operational lesson is simple: do not leave minimum-tax checks until final review week. Run the check early and store the evidence that supports your position. This includes turnover schedules, franked income support, and any exemption analysis used.

If your case involves incentives, losses, restructuring, or disputed classifications, escalate the minimum-tax analysis for specialist review.

- Commonly cited baseline: 0.5% of gross turnover less franked investment income.

- Exceptions and relief provisions can change the outcome materially.

- Check minimum tax in parallel with primary CIT computation.

What is the penalty for not filing CIT in Nigeria?

Late filing is costly and avoidable. Under commonly cited filing penalty provisions for company tax returns, failure to file can attract NGN 25,000 for the first month and NGN 5,000 for each subsequent month of default. Operational delays can also trigger additional interest, audit friction, and management escalation.

The best defense is timeline discipline. Build a reverse calendar from filing due date, assign named owners for schedules and reviews, and track completion status weekly near deadline. Most late filings happen because ownership is unclear, not because the tax team lacks technical skill.

For multi-entity groups, maintain one filing dashboard across all entities. Include return status, supporting schedules, reviewer, sign-off stage, and submission evidence.

- First month default is commonly cited at NGN 25,000.

- Each additional month is commonly cited at NGN 5,000.

- Use a reverse filing calendar with named owners.

Will Nigerian banks deduct 10% tax on foreign currency interest?

Many taxpayers ask this because they see 10% withholding in routine bank deductions. That pattern is common for interest income, but exemptions may apply for qualifying foreign-currency domiciliary account interest depending on legal conditions and taxpayer context. The right answer depends on documentation, not guesswork.

If deduction occurs and your technical position is exemption, preserve a complete trail: account type evidence, statement lines, legal clause, and tax reconciliation support. This gives your adviser what they need to evaluate credit or refund routes where applicable.

Avoid relying on social-media summaries for this topic. Use bank records and current legal references for the exact period under review.

- 10% withholding is common on many interest types.

- Some qualifying domiciliary interest may be exempt by statute.

- Reconcile every deduction against legal basis and documentation.

List of income exempted from tax in Nigeria: practical shortlist

Users often search for a complete list of income exempted from tax in Nigeria. The detail differs across company and personal tax frameworks, but a shortlist helps teams avoid obvious errors in early modeling. Typical high-impact categories include qualifying foreign-currency domiciliary account interest, relevant franked investment income treatment, and specific statutory exemptions tied to legislation or approved incentives.

Personal tax schedules may include additional exemptions for certain official emoluments, approved gratuities, or government securities where conditions are met. The key point is not memorizing a long list. The key point is linking each claimed exemption to a legal clause and a supporting document.

In audit practice, exemption claims fail most often because evidence is missing, not because the clause never existed.

- Map every exemption to clause, condition, and document.

- Separate company-tax exemptions from personal-tax exemptions.

- Keep exemption schedules with period-specific computations.

What is the tax free threshold in Nigeria? Also, salary example for NGN 300,000

There is no single tax-free threshold that answers every Nigerian tax question. For companies, threshold logic is linked to turnover, sector, and filing framework. For employees, threshold logic depends on personal reliefs and PAYE bands. Mixing those two systems produces confusion in both payroll and corporate planning discussions.

For the common search query how much tax is deducted from 300,000 salary in Nigeria, first define whether NGN 300,000 is monthly or annual. If it is monthly gross, annual gross is NGN 3.6 million. Under a simple PAYE illustration with standard relief assumptions, annual tax can be around NGN 560,000, roughly NGN 46,667 monthly before special adjustments.

Real payroll outcomes differ by pension treatment, statutory deductions, and employer compensation design. Always reconcile against payroll tax cards and monthly deduction records.

- Company threshold questions and salary threshold questions are different.

- NGN 300,000 monthly salary needs annualized PAYE analysis.

- Use payroll records for final deduction confirmation.

New tax law in Nigeria 2026 PDF download and document-control method

When searching for new tax law in Nigeria 2026 PDF download, prioritize official channels over reposts. Start with tax authority publications, National Assembly records, and official Gazette releases where available. Unverified file copies are a recurring source of wrong assumptions in corporate tax models.

After download, store each legal text with source URL, retrieval date, and checksum in your compliance repository. Keep related circulars in the same folder so interpretation notes remain attached to the primary text. This simple document-control process improves consistency across teams and reduces version disputes.

Methodology matters as much as content. This article was built by mapping the core decision first, then answering connected user questions in sequence, with examples, edge-case notes, and explicit uncertainty markers.

- Source legal PDFs from official institutions first.

- Archive each document with date, source, and checksum.

- Pair legal text with circulars used for implementation.

Final governance checks before sign-off

Before relying on any calculator output, run a short governance pass. Confirm turnover source, sector rationale, assessable-profit schedule, minimum-tax check, and filing timeline. Then verify who owns the final review and where evidence is archived. This takes minutes and prevents costly late-cycle reversals.

Teams that keep a one-page decision log for each run consistently perform better under review. A clean log should show assumptions, unresolved questions, reviewer names, and date-stamped updates.

If uncertainty remains material, escalate early. Fast escalation with organized records is always cheaper than post-filing correction.

- Evidence tie-out: turnover, sector, and assessable profit.

- Compliance tie-out: filing date, penalty exposure, minimum tax, and withholding.

- Ownership tie-out: named reviewers, dated assumptions, and archived files.

Deep-Dive Control Layer for 2026 CIT Screening

Treat this article as your decision map, then run a second-pass reconciliation before filing:

- tie turnover in your tax computation to bank-credit totals and invoicing ledgers

- document whether one-off proceeds are operational revenue or capital in nature

- record the reviewer who approved the threshold classification and date-stamp that decision

If your turnover lands near a boundary, compare this guide with What Happens When You Exceed the 0% CIT Threshold and How FIRS Verifies SME Zero-Tax Claims before submitting returns.

Evidence Matrix That Survives Review

A defensible file usually has four anchors:

- legal anchor: the rule you relied on, linked to Nigeria Revenue Service or FIRS CIT guidance

- data anchor: trial balance, bank extracts, invoice register, and adjustment notes

- behavior anchor: timely filing pattern, including nil years

- governance anchor: review notes, assumptions log, and approval trail

Case File: Borderline Year, Clean Outcome

An SME closed with turnover close to its internal threshold alert. Instead of force-fitting the result, the finance lead ran a three-scenario model, tagged uncertainties, and filed with a clear assumptions memo. The company paid what was due, defended every line item during routine queries, and avoided penalty accumulation.

People Also Ask

Nigeria 0% CIT threshold calculator: what does it check first?

It checks annual turnover and sector together. In this implementation, turnover at or below NGN 100 million with a non-Professional Services sector routes to the 0% CIT screening branch.

Company Income tax rate in Nigeria 2026: what percentage applies?

The percentage depends on the legal basis and company profile. Legacy references commonly show 0%, 20%, and 30% treatment bands, while this tool applies its configured 2026 screening model for first-pass decision support.

How to Calculate Company income tax in Nigeria?

Use tax-adjusted profit, determine assessable and taxable profit under your framework, apply the relevant rate or branch, then test minimum-tax and withholding interactions before final sign-off.

List of income exempted from tax in Nigeria?

A practical shortlist includes qualifying foreign-currency domiciliary account interest, franked investment income treatment in applicable contexts, and other statutory exemptions. Each item must be supported with legal and documentary evidence.

What is the tax free threshold in Nigeria?

There is no single threshold for all taxes. Company tax and personal income tax use different thresholds and methods. In this tool, threshold logic is company-focused and tied to turnover and sector.

How many percent is CIT tax in Nigeria?

It can vary by legal framework and company circumstances. Do not quote one percentage without naming the governing law and year. Use the current legal text and authority guidance for final filing.

Will Nigerian banks deduct 10% tax on foreign currency interest?

10% withholding is common for interest in many routine cases, but exemptions may apply for qualifying foreign-currency domiciliary interest. Confirm with account type evidence and legal references.

What is the penalty for not filing CIT in Nigeria?

A commonly cited framework is NGN 25,000 for the first month of default and NGN 5,000 for each additional month, with possible additional cost from delay and enforcement.

How much tax is deducted from 300,000 salary in Nigeria?

If NGN 300,000 is monthly gross salary, a simple annualized PAYE illustration can be around NGN 560,000 per year, roughly NGN 46,667 monthly before special deductions and payroll-specific adjustments.

How much is the minimum corporate income tax?

A commonly used baseline in practice is 0.5% of gross turnover less franked investment income, subject to statutory exceptions and transition rules that should be checked for the relevant year.

New tax law in Nigeria 2026 PDF download: where should I get it?

Start with official publication channels such as tax authority portals, National Assembly records, and official Gazette releases. Keep a dated internal copy with source and checksum.

Is the calculator output enough for final filing?

No. Use it for structured screening and planning. Final filing positions should be confirmed against current law, circulars, and adviser review where facts are complex.

Why does this tool ask for assessable profit separately?

Because assessable profit drives levy estimation when the high-turnover branch is active. It should not be inferred from turnover alone.

What should be archived after each calculator run?

Archive the generated report, input sheet, sector rationale, assessable-profit schedule, legal-reference note, and reviewer sign-off metadata.

What is the safest monthly process for keeping CIT screening accurate?

Update turnover and profit schedules monthly, rerun the calculator quarterly or after material changes, and maintain a dated decision log with assumptions and owners.

Sources and References

Continue reading

Explore other implementation notes in the blog or return to the tool suite.